Losing your job can feel like the floor has dropped out from under you, especially when you're facing unexpected expenses or trying to navigate financial difficulties. The thought of securing a personal loan during unemployment might seem like an impossible task, but understanding the factors involved can empower you to make informed decisions and explore available options.

The stress of unemployment is compounded by the worry of how to manage existing debts, cover essential bills, or handle emergency costs. When you're no longer receiving a regular paycheck, accessing credit can feel out of reach, leaving you unsure of where to turn for financial assistance. It's natural to feel overwhelmed and uncertain about your ability to qualify for a personal loan without a steady income.

Generally, a good to excellent credit score (670 or higher) significantly increases your chances of getting approved for a personal loan, even when unemployed. While a higher credit score doesn't guarantee approval, it demonstrates responsible credit management in the past and makes you a less risky borrower in the eyes of lenders. Lenders will also consider other factors like assets, savings, and potential sources of income. Some lenders might be willing to work with you if you have a strong credit history and can demonstrate the ability to repay the loan, even without a traditional job.

This article addresses the challenges of securing a personal loan while unemployed. We'll discuss the importance of credit score, alternative factors lenders consider, and strategies for improving your chances of approval. We'll also explore options like secured loans, co-signers, and alternative income sources. The goal is to provide you with a clear understanding of your options and equip you with the knowledge to navigate the lending landscape with confidence, even during periods of unemployment.

My Personal Experience and How It Relates

I remember when I was fresh out of college, working a freelance gig that was… let’s just say “unpredictable” in terms of income. I needed a small personal loan to consolidate some credit card debt. My credit score was decent, around 680, but my inconsistent income raised eyebrows with every lender I approached. I was constantly asked about my employment history and future income projections. It felt like I was being judged solely on my current situation, not on my past responsible credit behavior. One loan officer even suggested I get a co-signer, something I wasn't comfortable asking of my family at the time.

What I learned from that experience is that lenders are primarily concerned with risk. They need assurance that you can and will repay the loan. While a good credit score is a strong indicator of past responsibility, current income is a key factor in assessing future repayment ability. If you're unemployed, you need to find ways to mitigate that perceived risk. This could mean exploring secured loans, where you offer an asset as collateral, or finding a co-signer with a stable income and good credit history. It might also involve highlighting any alternative sources of income you have, such as investments, alimony, or even anticipated income from a new job offer.

The takeaway is that a good credit score is a fantastic foundation, but it's not the only piece of the puzzle. During unemployment, you need to proactively address lender concerns by demonstrating financial stability and a clear path to repayment. In my case, I ended up showcasing my freelance contracts and providing a detailed budget, which ultimately convinced a smaller credit union to approve my loan. It was a valuable lesson in understanding lender perspectives and proactively addressing their concerns.

What Exactly Does "Credit Score Needed" Mean in This Context?

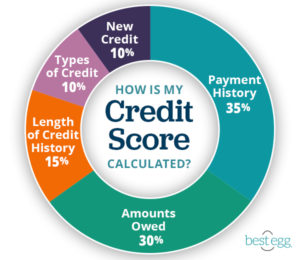

When we talk about the "credit score needed" for a personal loan while unemployed, we're essentially asking what numerical range of your credit report increases your chances of loan approval, even without a regular paycheck. Credit scores, most commonly FICO scores, range from 300 to 850, with higher scores indicating better creditworthiness. Lenders use these scores as a quick snapshot of your credit history, indicating how reliably you've managed debt in the past.

In the context of unemployment, your credit score becomes even more critical. A strong score signals to lenders that you have a history of responsible borrowing and repayment, making them more likely to overlook the temporary absence of income. A "good" credit score, generally considered to be between 670 and 739, opens doors to more favorable loan terms, lower interest rates, and higher approval odds. A "very good" score (740-799) or "excellent" score (800+) significantly increases your chances of securing a loan, even with limited or no current income.

However, it's essential to understand that the required credit score isn't a fixed number. It varies depending on the lender, the loan amount, and other factors like your debt-to-income ratio (if you have any income), your assets, and the overall economic climate. Some lenders specialize in working with borrowers who have less-than-perfect credit, but these loans often come with higher interest rates and fees. Knowing your credit score and understanding how lenders perceive it is the first step in navigating the personal loan process while unemployed. It allows you to target the right lenders and present yourself in the best possible light.

History and Myths Surrounding Credit Scores and Unemployment

The concept of credit scores emerged in the mid-20th century as a way to standardize lending decisions. Before that, loan approvals were often based on personal relationships and subjective assessments. The introduction of credit scoring systems, like FICO, brought a level of objectivity and efficiency to the lending process, allowing lenders to quickly assess risk based on statistical models.

One common myth is that unemployment automatically disqualifies you from getting a personal loan. While it certainly presents a challenge, it's not an insurmountable barrier. A strong credit history, combined with other positive financial factors, can often outweigh the lack of current employment. Another myth is that all lenders view unemployment the same way. In reality, different lenders have different risk tolerances and lending criteria. Some lenders specialize in working with borrowers who have non-traditional income sources or less-than-perfect credit.

Historically, obtaining a loan during unemployment was significantly more difficult due to limited access to credit information and more stringent lending practices. Today, with the rise of online lenders and alternative credit scoring models, there are more options available to borrowers who don't fit the traditional mold. However, it's crucial to be aware of predatory lenders who may take advantage of vulnerable individuals during periods of financial hardship. Always research lenders thoroughly and understand the terms and conditions of any loan before committing.

Hidden Secrets to Qualifying for a Personal Loan While Unemployed

One of the biggest "secrets" to getting a personal loan while unemployed is to proactively address the lender's concerns before they even ask. This means thoroughly documenting any alternative income sources you have. For example, if you're receiving unemployment benefits, provide proof of the benefit amount and duration. If you have investments, savings, or other assets, present statements that clearly show their value.

Another often-overlooked secret is the power of explanation. In your loan application or during your conversation with a loan officer, clearly articulate your situation and your plan for repayment. Explain why you're currently unemployed, what steps you're taking to find new employment, and how you intend to manage your loan payments. Transparency and honesty can go a long way in building trust and demonstrating your commitment to responsible borrowing.

Finally, consider exploring smaller, local lenders like credit unions or community banks. These institutions often have more flexibility in their lending criteria and may be more willing to consider your individual circumstances. They may also be more likely to offer personalized support and guidance throughout the application process. Building a relationship with a local lender can be a significant advantage when navigating the challenges of securing a personal loan during unemployment.

Recommendations for Securing a Loan When Unemployed

My top recommendation is to start by knowing your credit score. You can obtain free credit reports from Annual Credit Report.com. Understanding your credit score allows you to target lenders who cater to your specific credit profile. If your score is lower than ideal, focus on improving it before applying for a loan. This might involve paying down existing debt, correcting errors on your credit report, and avoiding new credit inquiries.

Another key recommendation is to explore secured loan options. A secured loan is backed by collateral, such as a car or savings account, which reduces the lender's risk and increases your chances of approval. While you risk losing your collateral if you default on the loan, secured loans often come with lower interest rates and more favorable terms than unsecured loans. Additionally, consider seeking a co-signer with a strong credit history and stable income. A co-signer guarantees the loan, making the lender more confident in your ability to repay.

Finally, be realistic about the loan amount you need. Borrowing more than you can comfortably repay will only increase your financial stress. Create a detailed budget that outlines your income, expenses, and potential loan payments. This will help you determine how much you can afford to borrow and ensure that you can meet your repayment obligations. Remember, a personal loan should be a tool to help you manage your finances, not a source of further financial strain.

Understanding Alternative Income Sources

When you're unemployed, traditional lenders often focus on the lack of a regular paycheck. That's why highlighting alternative income sources is crucial. This goes beyond simply stating you're receiving unemployment benefits. You need to provide documentation and context to demonstrate the reliability and sustainability of these income streams.

For instance, if you have investment income from stocks, bonds, or rental properties, gather statements that show consistent earnings over time. If you're receiving alimony or child support, provide court orders or payment records as proof. Even income from side hustles, freelance work, or gig economy jobs can be valuable. Document your earnings through invoices, bank statements, or tax returns. The key is to present a clear and convincing picture of your ability to generate income, even without a traditional employer.

Furthermore, be prepared to explain how these income sources will continue to support your loan repayment. Lenders want to see a stable and predictable income stream, regardless of its origin. By proactively showcasing your alternative income sources and demonstrating their reliability, you can significantly increase your chances of securing a personal loan while unemployed.

Tips for Improving Your Chances of Approval

One of the most effective tips is to reduce your debt-to-income ratio (DTI). Even if you're currently unemployed, lenders will still assess your existing debts relative to any income you may have. The lower your DTI, the more attractive you appear as a borrower. This means prioritizing paying down high-interest debt, such as credit card balances, before applying for a loan.

Another valuable tip is to carefully review your credit report for any errors or inaccuracies. Even minor mistakes can negatively impact your credit score. If you find any discrepancies, dispute them with the credit bureaus immediately. This can take time, so it's best to address any issues well in advance of applying for a loan. Furthermore, avoid opening new credit accounts or making large purchases on credit in the months leading up to your loan application. These actions can lower your credit score and signal financial instability to lenders.

Finally, be prepared to provide detailed documentation. Lenders will likely ask for proof of identity, residency, income, and assets. Gather all the necessary documents in advance to streamline the application process and demonstrate your preparedness. By taking these steps, you can significantly improve your chances of getting approved for a personal loan, even during periods of unemployment.

The Importance of a Co-Signer

Securing a co-signer can be a game-changer when applying for a personal loan while unemployed. A co-signer is someone who agrees to be responsible for repaying the loan if you are unable to do so. This reduces the lender's risk and significantly increases your chances of approval. Ideally, your co-signer should have a strong credit history, a stable income, and a low debt-to-income ratio.

However, it's crucial to choose your co-signer carefully and to have an open and honest conversation with them about the responsibilities involved. Make sure they understand that they are legally obligated to repay the loan if you default. Be prepared to provide them with all the information they need to make an informed decision, including the loan terms, interest rate, and repayment schedule. It's also important to have a plan in place in case you do encounter difficulties repaying the loan. This could involve setting aside funds in advance or exploring other options for financial assistance.

Remember, asking someone to be your co-signer is a big ask, and it can potentially strain your relationship if things go wrong. Therefore, it's essential to approach the situation with transparency, respect, and a clear understanding of the risks and responsibilities involved. If done correctly, securing a co-signer can be a valuable tool for accessing the credit you need during periods of unemployment.

Fun Facts About Credit Scores and Lending

Did you know that the FICO score, the most widely used credit score, was developed by Fair, Isaac and Company, now known as FICO, back in 1956? Initially, it was designed to predict the likelihood of individuals paying back their debts, and it has since become a cornerstone of the lending industry. Also, a surprisingly large number of Americans have never checked their credit score. Studies suggest that a significant percentage of the population remains unaware of their creditworthiness, which can hinder their ability to access credit and secure favorable loan terms.

Another interesting fact is that credit scores are not static; they fluctuate over time based on your credit behavior. Paying your bills on time, keeping your credit utilization low, and avoiding excessive credit inquiries can all positively impact your score. Conversely, late payments, high credit balances, and frequent applications for credit can negatively affect your score. Moreover, the factors that influence your credit score can vary depending on the scoring model used. While FICO is the most common, other models, such as Vantage Score, may weigh different factors differently. This means that your score can vary slightly depending on which model is used.

Finally, it's worth noting that credit scores are not the only factor that lenders consider. They also take into account your income, employment history, assets, and overall financial situation. While a good credit score is certainly an advantage, it's not the only determinant of loan approval. By understanding how credit scores work and how they fit into the broader lending process, you can make more informed decisions about your finances and improve your chances of accessing the credit you need.

How to Rebuild Your Credit After Unemployment

Rebuilding your credit after a period of unemployment can seem daunting, but it's definitely achievable with a strategic approach. The first step is to create a budget and stick to it. Identify areas where you can cut expenses and allocate those funds towards paying down debt. Even small payments can make a difference over time. Next, focus on paying all your bills on time, every time. Late payments can significantly damage your credit score, so prioritize staying current on your obligations.

Consider opening a secured credit card. These cards require a cash deposit as collateral, which reduces the risk for the lender. By making small purchases and paying them off on time each month, you can demonstrate responsible credit behavior and gradually rebuild your credit. Additionally, explore options for becoming an authorized user on someone else's credit card. If a friend or family member with a strong credit history adds you as an authorized user, their positive credit behavior can be reflected on your credit report.

Finally, be patient and persistent. Rebuilding credit takes time and effort. Don't get discouraged if you don't see results immediately. Stay focused on your goals, and continue practicing responsible credit habits. Over time, your credit score will improve, and you'll be able to access more favorable loan terms and financial opportunities.

What If You Can't Get a Personal Loan?

If you've explored all your options and still can't qualify for a personal loan, it's important not to despair. There are alternative strategies you can pursue to address your financial needs. One option is to explore government assistance programs, such as unemployment benefits, food stamps, or housing assistance. These programs can provide a temporary safety net while you search for employment and get back on your feet.

Another alternative is to seek help from non-profit credit counseling agencies. These agencies can provide free or low-cost financial advice, budget counseling, and debt management services. They can also help you negotiate with creditors to lower your interest rates or create a repayment plan that fits your budget. Additionally, consider reaching out to friends or family members for support. While it can be difficult to ask for help, a temporary loan from a trusted source may be a better option than resorting to high-interest payday loans or other predatory lending practices.

Finally, focus on developing new skills or pursuing alternative income streams. This could involve taking online courses, learning a new trade, or starting a side hustle. By investing in your skills and exploring new opportunities, you can increase your earning potential and improve your financial stability in the long run.

Listicle: 5 Ways to Boost Your Loan Approval Chances While Unemployed

1.Sharpen Your Credit Score: Before applying, obtain your credit report and address any errors. Pay down existing debt to improve your credit utilization ratio.

2.Gather Alternative Income Proof: Document any income sources, like unemployment benefits, investments, or freelance work. Provide statements to demonstrate consistent earnings.

3.Explore Secured Loan Options: Consider using assets like a car or savings account as collateral to reduce lender risk.

4.Secure a Reliable Co-Signer: Enlist the help of a friend or family member with a strong credit history and stable income.

5.Craft a Compelling Explanation: In your loan application, clearly articulate your unemployment situation, job search efforts, and repayment plan. Transparency builds trust.

Question and Answer

Q: What's the lowest credit score that might get approved?

A: While it's tough to give a definitive answer, some lenders might consider scores in the low to mid-600s, but expect higher interest rates and stricter terms.

Q: Besides my credit score, what else do lenders look at?

A: They'll consider any assets you have, alternative income sources (like unemployment benefits), and your overall debt-to-income ratio (if applicable).

Q: What if I have no income at all?

A: It's significantly harder, but not impossible. A secured loan or a co-signer with good credit can greatly improve your chances.

Q: Are there specific lenders that are more understanding of unemployment?

A: Yes, credit unions and smaller community banks often have more flexible lending criteria and may be willing to work with you on a personal level.

Conclusion of What credit score is needed to qualify for a personal loan if I am unemployed?

Securing a personal loan while unemployed is undoubtedly a challenge, but it's not an insurmountable one. A good to excellent credit score is a valuable asset, but it's not the only factor lenders consider. By proactively addressing lender concerns, exploring alternative income sources, and considering options like secured loans and co-signers, you can significantly improve your chances of approval. Remember to research lenders thoroughly, understand the loan terms, and prioritize responsible borrowing practices. With careful planning and a proactive approach, you can navigate the lending landscape with confidence, even during periods of unemployment.

Read Also: What are the eligibility criteria for a payday loan if I am currently unemployed?

Post a Comment