Facing unemployment is stressful enough, but when you need a personal loan on top of that, things can feel overwhelming. You're probably wondering if it's even possible to get approved, and what kind of credit score you'll need to make it happen. Let's break down the reality of securing a personal loan when you're out of work.

The prospect of borrowing money when you lack a steady income can be daunting. Lenders are naturally cautious, and it's understandable to feel like you're facing an uphill battle. Doubts about your ability to repay, coupled with the fear of rejection, can leave you feeling trapped and unsure where to turn.

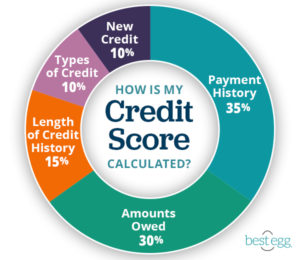

While there's no magic number, generally, a credit score of 660 or higher is preferable when seeking a personal loan while unemployed. Scores in the "good" (660-719) or "excellent" (720+) range significantly increase your chances. However, even with a score below 660, options might exist, albeit with potentially higher interest rates and stricter terms. Lenders will look at your complete financial picture, not just your credit score. Factors like assets, savings, and potential sources of income (like spousal support or investment income) will all be considered.

To sum up, securing a personal loan while unemployed hinges on your creditworthiness and overall financial stability. Aim for a credit score of 660 or higher, and be prepared to demonstrate your ability to repay the loan through alternative income sources or assets. Keywords like "unemployment," "personal loan," "credit score," and "alternative income" are crucial when researching your options.

Can I Get a Personal Loan with a Bad Credit Score When Unemployed?

Absolutely, this is a question that plagues many individuals in times of financial hardship. I remember when I was fresh out of college and struggling to find a job. My credit score wasn't stellar, hovering around the low 600s, and I needed a small personal loan to cover some unexpected medical expenses. I felt like the doors were slamming shut everywhere I turned. Traditional banks flat-out rejected my application, citing my lack of income and less-than-perfect credit history. It was incredibly disheartening and made me feel incredibly vulnerable.

However, I didn't give up. I started researching alternative lenders, those who specialize in working with individuals with less-than-ideal credit. These lenders often have higher interest rates, but they're more willing to consider factors beyond your credit score. They might look at your savings, assets, or potential co-signers. I eventually found a credit union that was willing to work with me because I had a small but consistent history of responsible credit usage, even with my low score. They also considered the fact that I was actively seeking employment and had a solid plan for repayment.

The key takeaway here is that a bad credit score doesn't automatically disqualify you from getting a personal loan when unemployed. It certainly makes the process more challenging, but it's not impossible. You'll need to be prepared to explore alternative lending options, potentially accept higher interest rates, and demonstrate your ability to repay the loan through other means. Building and maintaining any credit is essential, and so is knowing that the minimum is 660 or higher, because credit scores can be important to get approval.

What Factors Do Lenders Consider Besides Credit Score?

Lenders don't solely rely on your credit score when evaluating your loan application, especially when you're unemployed. They want a comprehensive picture of your financial situation and your ability to repay the loan. The minimum credit score needed can vary widely, so lenders must look at other factors.

One crucial factor is your debt-to-income ratio (DTI), even if your income is currently zero. They'll assess your existing debts, such as credit card balances, student loans, or car payments, and compare them to any income you might have from sources like unemployment benefits, spousal support, investment income, or even a side hustle. A lower DTI demonstrates that you're not overly burdened by debt and have a greater capacity to take on a new loan.

Lenders also consider your assets. Do you own a home, have savings accounts, or possess valuable investments? These assets can serve as collateral or demonstrate your financial stability. Even a modest emergency fund can signal to a lender that you're prepared for unexpected expenses and are less likely to default on your loan. Finally, the loan amount you're requesting matters. Smaller loans are generally easier to obtain than larger ones, as they represent less risk for the lender. So, be realistic about how much you truly need and avoid borrowing more than you can comfortably repay, even with alternative income streams. Remember, lenders are looking for evidence of responsible financial behavior and the ability to manage your debt, regardless of your employment status.

The History and Myth of Credit Scores and Unemployment

The concept of credit scores is relatively modern, emerging in the mid-20th century. Before that, lenders relied on personal relationships and subjective assessments to determine creditworthiness. The rise of credit scoring algorithms, like FICO, aimed to provide a more objective and standardized measure of risk. However, these algorithms weren't designed to account for unique situations like unemployment.

A common myth is that unemployment automatically disqualifies you from getting a loan. While it certainly presents a challenge, it's not an insurmountable barrier. Lenders understand that job loss can happen to anyone, and they're willing to consider other factors that demonstrate your ability to repay. The myth perpetuates the idea that the credit system is inflexible and unforgiving, which isn't entirely true. Alternative lending options and a strong financial profile can still open doors. Another myth is that a high credit score guarantees loan approval, even without income. While a good credit score is essential, it's only one piece of the puzzle. Lenders need to be confident that you can repay the loan, regardless of your credit history. A high score without a source of income might still lead to rejection.

The truth lies somewhere in between. Credit scores play a significant role in lending decisions, but they're not the sole determinant, especially during periods of unemployment. Understanding the history of credit scoring and debunking common myths can empower you to navigate the lending landscape more effectively and explore all available options.

The Hidden Secrets to Getting Approved Despite Unemployment

While lenders publicly state the factors they consider, some less obvious strategies can significantly improve your chances of getting approved for a personal loan while unemployed. One "secret" is to focus on improving your credit utilization ratio. This ratio represents the amount of credit you're using compared to your total available credit. Keeping this ratio low, ideally below 30%, demonstrates responsible credit management and makes you a more attractive borrower, even without a steady income. Another often-overlooked aspect is building relationships with local banks or credit unions. These institutions are often more willing to consider individual circumstances and offer personalized solutions compared to large national lenders. By establishing a rapport and explaining your situation honestly, you might find them more receptive to your loan application. A third "secret" is to be proactive in documenting any potential income sources. Gather statements from investment accounts, rental properties, or any other assets that generate income. Providing this documentation upfront demonstrates your ability to repay the loan and alleviates the lender's concerns.

Moreover, consider consolidating existing debt before applying for a personal loan. By consolidating high-interest debts into a single, lower-interest loan, you can free up cash flow and improve your DTI, making you a more appealing borrower. The key is to present yourself as a responsible and resourceful individual who is actively managing their finances despite the challenges of unemployment. Showing initiative and transparency can go a long way in securing loan approval.

Recommendations for Securing a Personal Loan While Unemployed

If you're facing unemployment and need a personal loan, don't despair. Several strategies can increase your chances of success. First, meticulously review your credit report and address any errors or inaccuracies. Disputing errors can improve your credit score and make you a more attractive borrower. Secondly, explore secured personal loans. These loans require you to pledge an asset as collateral, such as a car or savings account. The collateral reduces the lender's risk, making them more willing to approve your application, even with a lower credit score or lack of income. However, you will want to aim for a credit score of 660 or higher.

Thirdly, consider applying for a loan with a co-signer. A co-signer is someone with a strong credit history and stable income who agrees to be responsible for the loan if you default. This significantly reduces the lender's risk and increases your chances of approval. However, be sure to choose a co-signer who understands the risks involved and is willing to take on that responsibility. Fourthly, thoroughly research different lenders and compare their terms and conditions. Look for lenders who specialize in working with individuals with less-than-perfect credit or who offer alternative lending options. Finally, be prepared to provide comprehensive documentation of your financial situation, including income sources, assets, and expenses. Transparency and honesty are crucial when applying for a loan while unemployed.

Understanding Different Types of Personal Loans Available

The world of personal loans isn't a one-size-fits-all scenario. Understanding the different types of loans available is crucial, especially when navigating the challenges of unemployment. Secured personal loans, as mentioned earlier, require collateral, providing lenders with a safety net and potentially leading to more favorable terms. Unsecured personal loans, on the other hand, don't require collateral but typically come with higher interest rates and stricter eligibility requirements. Then there are debt consolidation loans, designed specifically to combine multiple debts into a single, more manageable loan. These can be helpful if you're struggling to keep up with various payments and want to simplify your finances.

Another type is a credit-builder loan, which is designed to help individuals with limited or poor credit establish a positive credit history. These loans often involve borrowing a small amount of money and making regular payments over a set period, with the funds held in a secured account until the loan is repaid. Finally, some lenders offer specialized personal loans for specific purposes, such as home improvement, medical expenses, or education. These loans may have more flexible terms or lower interest rates compared to general-purpose personal loans. When choosing a personal loan, carefully consider your individual needs and financial situation. Research different lenders, compare their terms and conditions, and choose the loan that best aligns with your goals and your ability to repay. Remember that even with a lower credit score or unemployment, options exist, but careful planning and research are essential.

Top Tips for Improving Your Chances of Loan Approval

Securing a personal loan when you're unemployed requires a proactive and strategic approach. One of the most effective tips is to actively work on improving your credit score. Even small improvements can make a difference. Pay down existing debt, especially credit card balances, to lower your credit utilization ratio. Make all your payments on time, as even a single missed payment can negatively impact your credit score. Also, you should aim for a credit score of 660 or higher for better approval chances.

Another crucial tip is to gather comprehensive documentation of your financial situation. This includes bank statements, investment account statements, and any proof of income from sources like unemployment benefits, spousal support, or rental properties. Presenting a clear and organized picture of your finances demonstrates responsibility and increases the lender's confidence in your ability to repay. Also, consider exploring alternative lending options. Credit unions, online lenders, and peer-to-peer lending platforms may be more willing to work with individuals who don't meet the traditional requirements of banks. These lenders often have more flexible eligibility criteria and may offer specialized loans for specific situations. Finally, be prepared to explain your situation honestly and transparently to the lender. Explain why you're unemployed, what steps you're taking to find a new job, and how you plan to repay the loan. Transparency and a proactive attitude can go a long way in securing loan approval.

Navigating the Application Process: What to Expect

The personal loan application process can seem daunting, especially when you're unemployed. However, understanding what to expect can alleviate anxiety and increase your chances of success. The first step is to gather all the necessary documentation. This typically includes identification, proof of address, bank statements, and any documentation of income or assets. Next, you'll need to complete the loan application, either online or in person. Be sure to answer all questions honestly and accurately, and double-check for any errors before submitting. The lender will then review your application and conduct a credit check. They may also request additional information or documentation to verify your financial situation.

If your application is approved, the lender will present you with a loan agreement outlining the terms and conditions of the loan, including the interest rate, repayment schedule, and any fees. Carefully review the agreement before signing, and don't hesitate to ask questions if anything is unclear. Once you sign the agreement, the loan funds will typically be deposited into your bank account within a few days. Be sure to keep track of your repayment schedule and make all payments on time to avoid late fees and negative impacts on your credit score. Remember that the application process can vary depending on the lender and the type of loan you're applying for. Research different lenders and understand their specific requirements before starting the process. If you have any concerns or questions, don't hesitate to seek guidance from a financial advisor.

Fun Facts About Personal Loans

Did you know that the first personal loan was likely a handshake agreement between family members or friends? The concept of lending money for personal use has been around for centuries, but the formalization of personal loans as we know them today is a relatively recent development. Another fun fact is that the average personal loan amount in the United States is around $16,000. However, loan amounts can range from a few hundred dollars to tens of thousands of dollars, depending on the lender, the borrower's creditworthiness, and the purpose of the loan.

It's also interesting to note that the interest rates on personal loans can vary widely depending on factors such as the borrower's credit score, the loan amount, and the loan term. Interest rates can range from single digits for borrowers with excellent credit to over 30% for borrowers with poor credit. Another surprising fact is that many people use personal loans for unexpected expenses, such as medical bills, car repairs, or home repairs. These loans can provide a much-needed source of funds during times of financial hardship. Finally, it's worth noting that personal loans can be used for a wide variety of purposes, from debt consolidation to home improvement to vacation planning. The flexibility of personal loans makes them a popular choice for many borrowers.

How to Negotiate Better Loan Terms

Negotiating better loan terms can save you money and make your loan more manageable. One effective strategy is to shop around and compare offers from different lenders. Get quotes from multiple banks, credit unions, and online lenders, and compare the interest rates, fees, and repayment terms. Having multiple offers gives you leverage to negotiate better terms with your preferred lender. Another tip is to improve your credit score before applying for a loan. Even a small improvement can qualify you for a lower interest rate.

Pay down existing debt, correct any errors on your credit report, and make all your payments on time. Also, consider offering collateral to secure the loan. Secured loans typically have lower interest rates than unsecured loans because the lender has less risk. Be prepared to explain your situation to the lender and demonstrate your ability to repay the loan. Provide documentation of your income, assets, and expenses, and be honest about your financial situation. Finally, don't be afraid to walk away if you're not happy with the loan terms. There are many lenders out there, and you should choose the one that offers the best terms for your individual needs. Remember that negotiation is a key part of the loan process, and you have the right to advocate for yourself.

What If I Am Denied a Personal Loan?

Being denied a personal loan can be discouraging, but it's not the end of the road. The first step is to find out why your application was denied. The lender is legally required to provide you with a reason for the denial, which may be related to your credit score, income, debt, or other factors. Once you know the reason, you can take steps to address the issue.

If your denial was due to a low credit score, focus on improving your credit. Pay down existing debt, correct any errors on your credit report, and make all your payments on time. If your denial was due to insufficient income, explore ways to increase your income, such as taking on a part-time job or selling assets. You can also consider applying for a loan with a co-signer who has a strong credit history and stable income. Another option is to explore alternative lending options, such as credit unions or peer-to-peer lending platforms. These lenders may be more willing to work with individuals who don't meet the traditional requirements of banks. Finally, don't give up. Keep working to improve your financial situation and reapply for a loan when you're in a stronger position. Remember that denial is not a reflection of your worth, but rather an opportunity to learn and grow.

Top 5 Things to Know About Personal Loans When Unemployed (Listicle)

When facing unemployment, navigating the world of personal loans can feel overwhelming. Here's a listicle of the top 5 things you need to know: 1. Credit Score Matters, But It's Not Everything: While a good credit score (aim for 660 or higher) increases your chances, lenders also consider other factors like assets and alternative income sources.

2. Explore Secured Loans: Offering collateral, like a car or savings account, reduces the lender's risk and makes you a more attractive borrower.

3. Co-signers Can Help: A co-signer with a strong credit history can significantly improve your chances of approval.

4. Shop Around and Compare Offers: Don't settle for the first offer you receive. Compare terms from multiple lenders to find the best deal.

5. Be Transparent and Honest: Provide accurate information and explain your situation clearly to the lender. Honesty builds trust and increases your chances of success.

Question and Answer about What is the minimum credit score needed to get a personal loan if I am unemployed?

Q: What is the absolute minimum credit score I can have and still potentially get a personal loan while unemployed?

A: While it's difficult to pinpoint an exact number, some lenders may consider applicants with credit scores in the low 600s, but approval is far from guaranteed and will likely come with higher interest rates and stricter terms. You'll need a strong overall financial profile to compensate.

Q: What if I have no credit history at all? Can I still get a personal loan?

A: It's very challenging to get a personal loan with no credit history, as lenders have no way to assess your creditworthiness. Consider building credit first by getting a secured credit card or becoming an authorized user on someone else's card.

Q: What are some examples of "alternative income" that lenders might consider?

A: Alternative income can include unemployment benefits, spousal support, investment income, rental income, Social Security benefits, or income from a side hustle or freelance work. Be prepared to provide documentation of these income sources.

Q: How much higher will interest rates be if I have a lower credit score?

A: Interest rates can be significantly higher for borrowers with lower credit scores. The difference can be several percentage points, which can add up to hundreds or even thousands of dollars over the life of the loan. It's crucial to compare offers carefully and understand the total cost of the loan.

Conclusion of What is the minimum credit score needed to get a personal loan if I am unemployed?

Securing a personal loan while unemployed presents unique challenges, but it's not an impossible feat. While a credit score of 660 or higher is generally recommended, alternative options exist for those with lower scores. Focus on improving your credit, exploring secured loans, considering a co-signer, and demonstrating your ability to repay through alternative income sources or assets. Remember to shop around, compare offers, and be transparent with lenders. By taking a proactive and strategic approach, you can increase your chances of securing the financial assistance you need during this challenging time.

Post a Comment