Life throws curveballs, doesn't it? One minute you're sailing along, and the next, an unexpected expense crashes into your finances. It's in these moments, when emergency benefits aren't quite enough, that the idea of a supplemental loan starts to glimmer with hope. But what does that process actually look like?

Navigating financial emergencies is stressful enough without adding layers of complex paperwork and confusing requirements. Figuring out where to even begin, let alone understand the eligibility criteria and documentation needed, can feel overwhelming. The thought of rejection, the potential impact on your credit score, and the added debt can keep you up at night.

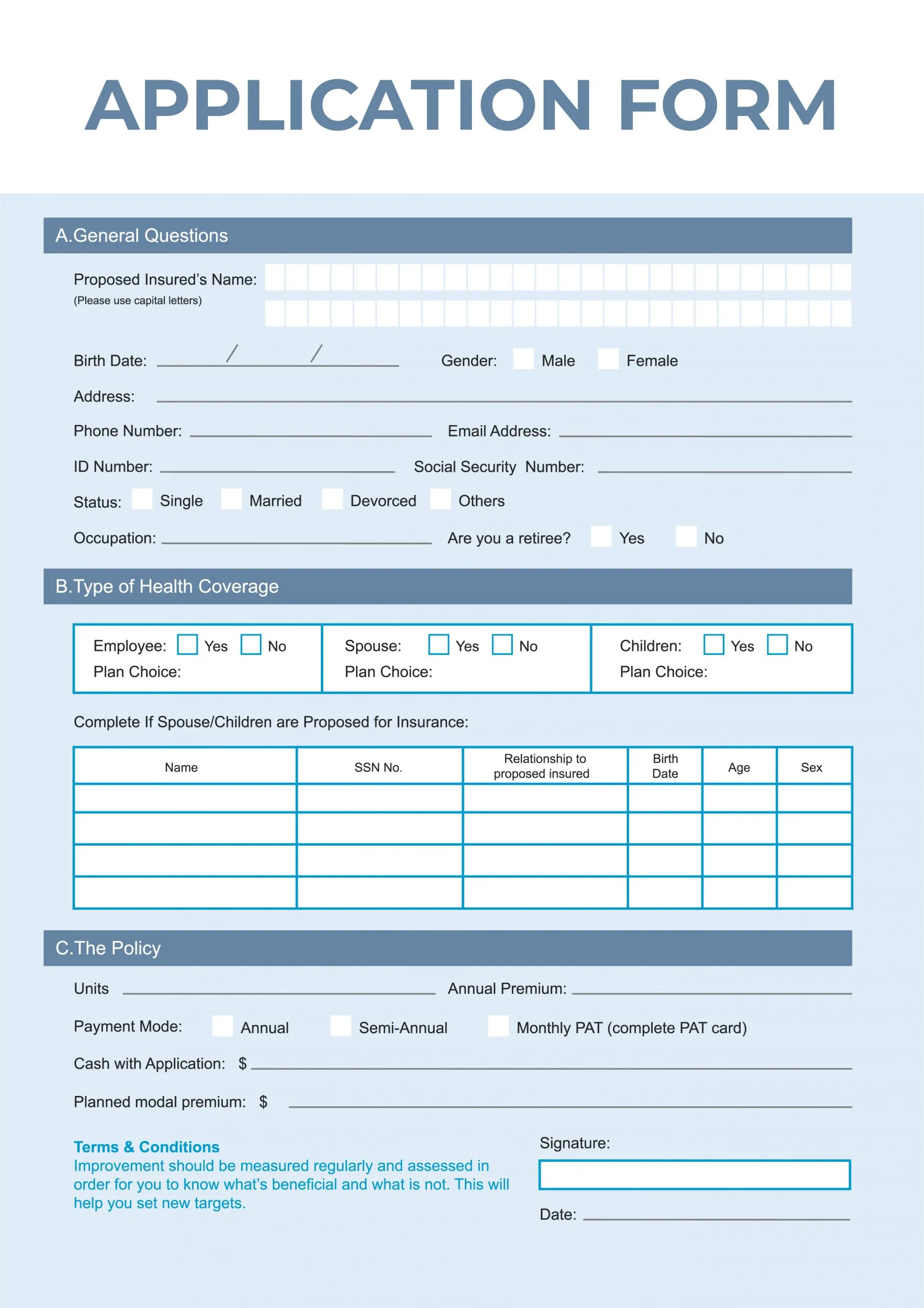

The application process for a supplemental loan for emergency benefits typically involves several steps. First, you need to research and identify lenders that offer these types of loans. Credit unions, banks, and online lenders are common sources. Next, you'll need to determine if you meet the lender's eligibility criteria, which usually includes factors like credit score, income, and debt-to-income ratio. You'll then need to gather the required documentation, such as proof of income, identification, and details about your emergency and existing benefits. After completing the application, the lender will review it and may request additional information. If approved, you'll receive the loan terms, including the interest rate and repayment schedule. Finally, you'll need to sign the loan agreement, and the funds will be disbursed to you.

In short, securing a supplemental loan for emergency benefits involves research, eligibility checks, documentation, application, review, and acceptance. Understanding this process is crucial to navigating unexpected financial hardships and finding the right support when you need it most. Knowing where to look, what to expect, and how to prepare can significantly ease the stress of seeking financial assistance during a crisis. Keywords to keep in mind include: emergency loans, supplemental loans, emergency benefits, loan application, eligibility criteria, and financial assistance.

Understanding Eligibility Requirements

I remember a time when my car broke down unexpectedly, and I was relying on unemployment benefits to get by. The repairs were far more expensive than I anticipated, and my benefits simply weren't enough. I started looking into supplemental loans, but the eligibility requirements seemed daunting. One lender required a credit score I didn't have, another demanded proof of stable employment, which was impossible given my situation. It felt like I was hitting wall after wall.

Eventually, I found a local credit union that was willing to consider my application based on my overall financial situation and the specifics of my emergency. They took the time to understand my circumstances and offered a loan with reasonable terms. This experience taught me the importance of researching lenders thoroughly and understanding their eligibility criteria upfront. Each lender has its own set of requirements, and finding one that aligns with your specific situation is key. For example, some lenders specialize in working with individuals receiving government benefits, while others may have more stringent credit score requirements. Always check the fine print and don't be afraid to ask questions to ensure you fully understand the criteria before applying. Furthermore, consider that lenders often have age, citizenship, and residency requirements, as well as proof of identity.

Gathering Necessary Documentation

The application process for a supplemental loan requires you to prove you are who you say you are, and that you need the money that you say you do. The documents required can vary depending on the lender, but typically include proof of identity (such as a driver's license or passport), proof of income (pay stubs, tax returns, or bank statements), and documentation of your emergency (repair bills, medical invoices, or eviction notices). Some lenders may also require proof of your existing emergency benefits, such as award letters or payment statements. Having all of these documents readily available will streamline the application process and increase your chances of approval.

It's also a good idea to gather any additional documentation that could strengthen your application, such as letters of support from family or friends, or a written explanation of your financial situation. Lenders want to see that you are responsible and committed to repaying the loan, and providing additional context can help them assess your creditworthiness. Remember, the more prepared you are, the smoother the application process will be. Make copies of all your documents and keep them organized so you can easily access them when needed. This will not only save you time but also demonstrate to the lender that you are serious about obtaining the loan and managing your finances responsibly.

History and Myths Surrounding Emergency Loans

The history of emergency loans dates back centuries, with early forms of lending often provided by community members or religious institutions. Over time, formal financial institutions began offering loans to individuals facing unexpected hardships. Today, emergency loans are a common financial product, available from a wide range of lenders.

However, there are also many myths surrounding emergency loans. One common myth is that emergency loans are always predatory and should be avoided at all costs. While it's true that some lenders charge exorbitant interest rates and fees, there are also many reputable lenders that offer fair and affordable loans. Another myth is that emergency loans are only for people with bad credit. In reality, people of all credit scores can experience financial emergencies and may need to turn to loans for assistance. The key is to research lenders carefully and choose one that offers terms that you can afford. Additionally, some believe that obtaining a supplemental loan will negatively impact their chances for approval for further social safety net benefits, which is not necessarily the case. Many organizations recognize that an emergency loan can be part of a responsible response to unforeseen circumstances, when managed effectively.

Unveiling Hidden Secrets of Supplemental Loan Applications

One of the best-kept secrets about supplemental loan applications is the power of negotiation. Many borrowers don't realize that they can negotiate the terms of the loan, such as the interest rate, repayment schedule, or fees. If you have a strong credit history or can provide collateral, you may be able to negotiate a lower interest rate. Similarly, if you need a longer repayment period to make the loan more affordable, you can try to negotiate this with the lender. Don't be afraid to advocate for yourself and ask for terms that work for you.

Another secret is the importance of comparison shopping. Don't settle for the first loan offer you receive. Shop around and compare offers from multiple lenders to find the best terms and rates. Use online comparison tools to quickly compare loan options and identify the most favorable deals. Remember, even a small difference in the interest rate can save you a significant amount of money over the life of the loan. Moreover, look for lenders who are transparent about their fees and charges. Some lenders may try to hide fees or include them in the fine print. Make sure you understand all the costs associated with the loan before you agree to it. By being informed and proactive, you can increase your chances of getting a supplemental loan with terms that are fair and affordable.

Recommendations for a Smooth Application Process

Based on my experience and research, I can offer some recommendations for a smooth application process for a supplemental loan for emergency benefits. First, start by assessing your financial situation and determining how much money you actually need. Don't borrow more than you can afford to repay. Next, research lenders and compare their eligibility requirements, interest rates, fees, and repayment terms. Choose a lender that offers terms that align with your needs and financial situation.

Gather all the necessary documentation before you start the application process. This will save you time and prevent delays. When filling out the application, be honest and accurate. Provide complete and truthful information about your income, expenses, and debts. If you have any questions or concerns, don't hesitate to contact the lender and ask for clarification. Finally, review the loan agreement carefully before you sign it. Make sure you understand all the terms and conditions, including the interest rate, repayment schedule, and any fees or penalties. If you're not comfortable with any of the terms, don't hesitate to negotiate or seek a different loan. By following these recommendations, you can increase your chances of getting a supplemental loan with terms that are manageable and affordable.

Navigating Online Loan Applications

The digital age has brought loan applications to our fingertips, making the process more accessible and convenient. However, it's essential to navigate online loan applications with caution and awareness. Before diving in, verify the legitimacy of the online lender. Look for reputable lenders with secure websites, clear contact information, and positive customer reviews. Be wary of lenders that promise guaranteed approval or require upfront fees.

When filling out an online loan application, protect your personal information by using a secure internet connection and creating strong passwords. Read the lender's privacy policy to understand how your information will be used and shared. Be cautious about clicking on suspicious links or providing sensitive information to unknown sources. If you're unsure about a lender's legitimacy, check with the Better Business Bureau or the Consumer Financial Protection Bureau. Additionally, remember to keep a record of all your online communications and application details. This will help you track your progress and protect yourself in case of any disputes. By following these tips, you can navigate online loan applications safely and effectively, increasing your chances of finding the right supplemental loan for your emergency needs.

Tips for a Successful Supplemental Loan Application

Securing a supplemental loan when you're already relying on emergency benefits can feel like a tightrope walk. Here are some tips to increase your chances of approval and ensure you're making the right financial decision.

First, improve your credit score if possible. Even small improvements can make a big difference in your eligibility and the interest rate you receive. Pay down existing debts, correct any errors on your credit report, and avoid taking on new debt before applying. Second, demonstrate your ability to repay the loan. Show the lender that you have a plan for managing your finances and making timely payments. This could include creating a budget, cutting expenses, or seeking additional income. Third, consider a secured loan. If you have assets such as a car or savings account, you may be able to secure the loan with these assets, which can lower the interest rate and increase your chances of approval. Finally, be prepared to explain your emergency and how the loan will help you resolve it. The more clearly you can articulate your situation, the more likely the lender is to understand your needs and approve your application.

Understanding Interest Rates and Fees

Navigating the world of interest rates and fees can be overwhelming, but understanding these costs is crucial for making informed decisions about supplemental loans. Interest rates are the percentage of the loan amount that you'll be charged for borrowing the money. They can be fixed or variable, and they can vary significantly depending on the lender, your credit score, and the type of loan.

Fees are additional charges that the lender may impose, such as origination fees, application fees, or prepayment penalties. Always ask the lender to disclose all fees upfront and factor them into the total cost of the loan. When comparing loan offers, focus on the annual percentage rate (APR), which includes both the interest rate and the fees. This will give you a more accurate picture of the true cost of the loan. Also, be aware of prepayment penalties, which are fees charged if you pay off the loan early. If you anticipate being able to repay the loan before the end of the term, choose a loan with no prepayment penalty. By understanding interest rates and fees, you can make a more informed decision about which supplemental loan is right for you and avoid costly surprises down the road.

Fun Facts About Emergency Loans

Did you know that the concept of emergency loans dates back to ancient civilizations? In ancient Rome, wealthy citizens would often provide loans to those in need, albeit with varying levels of generosity. Today, the emergency loan market is a multi-billion dollar industry, with a diverse range of lenders and loan products available.

Another fun fact is that the average emergency loan amount is around $1,000. This amount is often enough to cover unexpected expenses such as car repairs, medical bills, or home repairs. However, some people may need to borrow more or less depending on their specific circumstances. Interestingly, the approval rate for emergency loans is generally lower than for other types of loans, such as mortgages or auto loans. This is because lenders perceive emergency loans as riskier, due to the borrower's urgent need for funds. Despite the challenges, emergency loans can be a valuable resource for those facing unexpected financial hardships. By understanding the history, statistics, and realities of emergency loans, you can approach the application process with greater confidence and make informed decisions about your financial future.

How To Choose the Right Lender

Choosing the right lender for a supplemental loan is a critical step in ensuring you get the financial assistance you need without falling into a cycle of debt. Start by researching different types of lenders, including banks, credit unions, and online lenders. Each type of lender has its own advantages and disadvantages. Banks may offer lower interest rates but have stricter eligibility requirements. Credit unions may be more willing to work with borrowers who have less-than-perfect credit. Online lenders may offer faster approval and funding, but their interest rates may be higher.

Once you've identified a few potential lenders, compare their eligibility requirements, interest rates, fees, and repayment terms. Look for lenders that are transparent about their fees and charges and offer loan terms that you can afford. Read online reviews and check with the Better Business Bureau to get a sense of the lender's reputation and customer service. Also, consider the lender's customer service and support. Do they offer multiple ways to contact them, such as phone, email, or chat? Are their representatives knowledgeable and helpful? A good lender will be responsive to your questions and concerns and provide clear and accurate information about the loan. By taking the time to research and compare lenders, you can increase your chances of finding the right loan for your needs and avoid the pitfalls of predatory lending.

What If Your Loan Application Is Denied?

Rejection can sting, especially when you're already facing a financial emergency. If your application for a supplemental loan is denied, don't despair. Instead, take it as an opportunity to understand why you were denied and take steps to improve your chances of approval in the future. Start by asking the lender for the specific reasons for the denial. Under the Fair Credit Reporting Act, you're entitled to this information.

Common reasons for loan denial include a low credit score, high debt-to-income ratio, or insufficient income. Once you know the reasons for the denial, you can take steps to address them. Improve your credit score by paying down debts, correcting errors on your credit report, and avoiding new debt. Lower your debt-to-income ratio by paying off debts or increasing your income. If your income is insufficient, consider seeking additional employment or exploring other sources of income. You can also try applying for a loan with a co-signer or securing the loan with collateral. Finally, don't be afraid to shop around and apply with multiple lenders. Each lender has its own eligibility requirements and may be more willing to work with you than others. By understanding the reasons for the denial and taking steps to improve your financial situation, you can increase your chances of getting approved for a supplemental loan in the future.

Listicle: 5 Steps to Prepare for a Supplemental Loan Application

Applying for a supplemental loan can be stressful, but with the right preparation, you can increase your chances of success. Here are five key steps to take before you apply:

1.Assess Your Financial Situation: Understand your income, expenses, debts, and credit score. This will help you determine how much you need to borrow and what you can afford to repay.

2.Research Lenders: Compare different types of lenders, such as banks, credit unions, and online lenders. Look at their eligibility requirements, interest rates, fees, and repayment terms.

3.Gather Documentation: Collect all the necessary documents, such as proof of income, identification, and documentation of your emergency. Having these documents ready will streamline the application process.

4.Improve Your Credit Score: Take steps to improve your credit score, such as paying down debts and correcting errors on your credit report. Even small improvements can make a big difference.

5.Create a Budget: Develop a budget to demonstrate your ability to repay the loan. Show the lender that you have a plan for managing your finances and making timely payments.

Question and Answer Section

Q: What is the typical interest rate for a supplemental loan for emergency benefits?

A: Interest rates vary widely depending on the lender, your credit score, and the loan terms. They can range from a few percentage points to over 30%. It's essential to compare rates from multiple lenders to find the best deal.

Q: Can I get a supplemental loan if I have bad credit?

A: It may be more challenging, but not impossible. Some lenders specialize in working with borrowers who have bad credit. However, be prepared for higher interest rates and fees.

Q: What if I can't repay the loan?

A: Contact the lender immediately and explain your situation. They may be willing to work with you on a payment plan or offer other options. Ignoring the problem can lead to late fees, damage to your credit score, and even legal action.

Q: How long does it take to get approved for a supplemental loan?

A: Approval times vary depending on the lender and the complexity of your application. Some lenders offer instant approval, while others may take a few days or even weeks to process your application.

Conclusion of What is the application process for a supplemental loan for emergency benefits?

Navigating the application process for a supplemental loan during a financial emergency can feel overwhelming. However, by understanding the steps involved, gathering the necessary documentation, and researching your options, you can increase your chances of securing the financial assistance you need. Remember to compare lenders, negotiate terms, and always prioritize responsible borrowing. While supplemental loans can provide a lifeline during difficult times, they should be approached with caution and a clear understanding of the terms and conditions. By being informed and proactive, you can navigate the process successfully and regain control of your financial future.

Post a Comment